GoTyme Bank permanently discontinued its popular “cash‑in via linked bank account” feature, ending a convenience tool that allowed users to deposit directly from BPI, UnionBank, Chinabank, and RCBC accounts inside the app. The move takes effect February 1, 2026, and comes after weeks of confusion among customers who initially saw the service marked as “on maintenance” through late January.

![]()

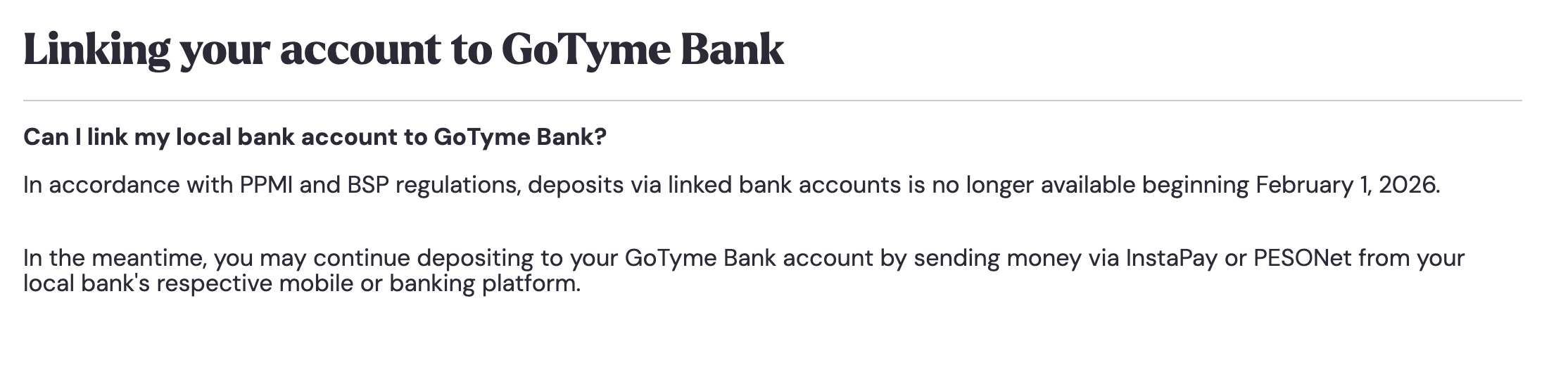

In an updated help page, GoTyme states that “in accordance with PPMI and BSP regulations, deposits via linked bank accounts is no longer available beginning February 1, 2026.” Instead, the Gokongwei‑backed digital bank is directing users to fund their accounts by sending money via InstaPay or PESONet from their other bank’s own mobile channels, or by using partner cash‑in points such as 7‑Eleven.

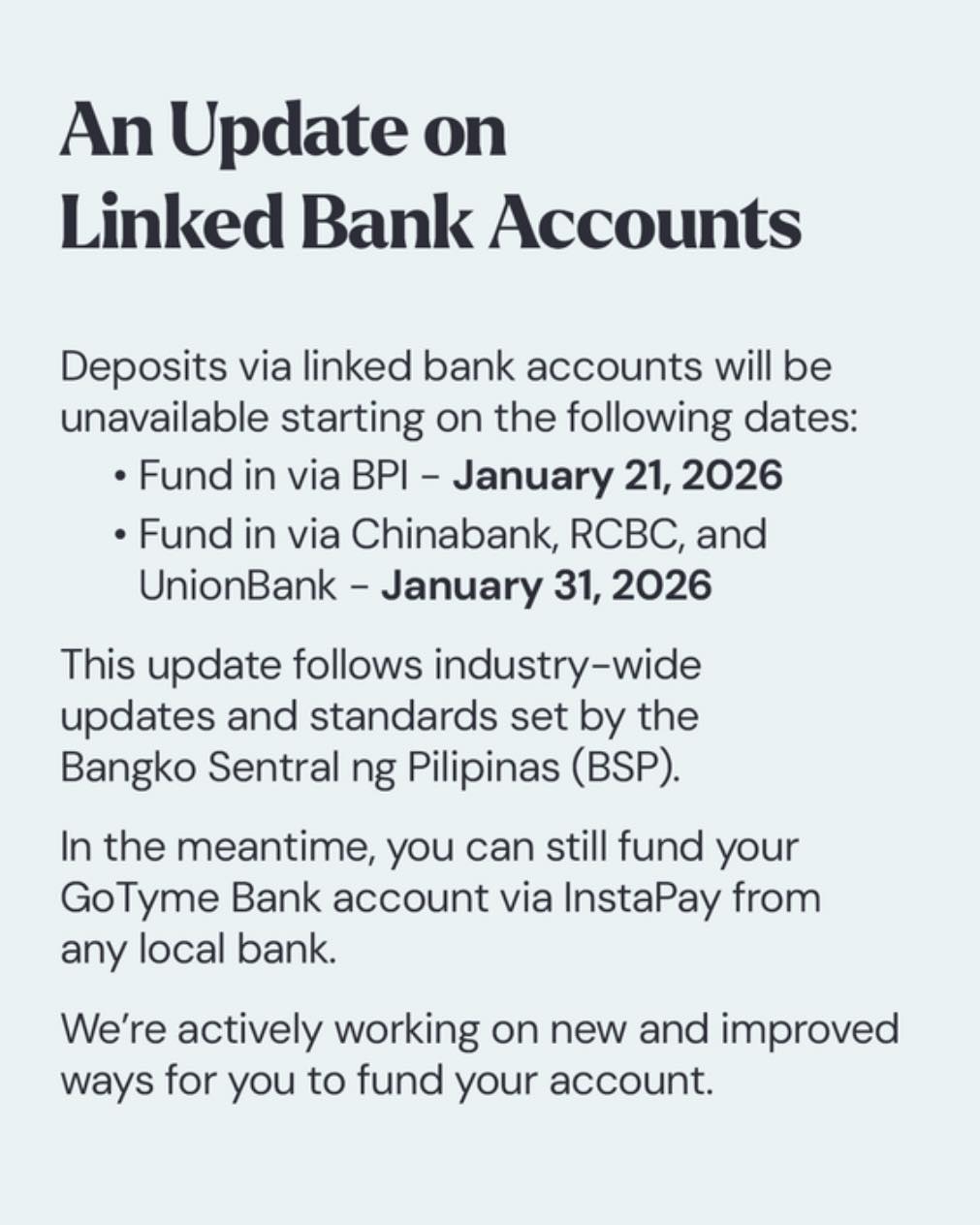

The change follows a series of advisories circulated in mid‑January, where GoTyme and community channels warned that deposits via bank accounts would soon be disabled. Funding from BPI was scheduled to stop on January 21, with deposits from other linked banks ending January 31, effectively phasing out the feature ahead of the February cutoff.

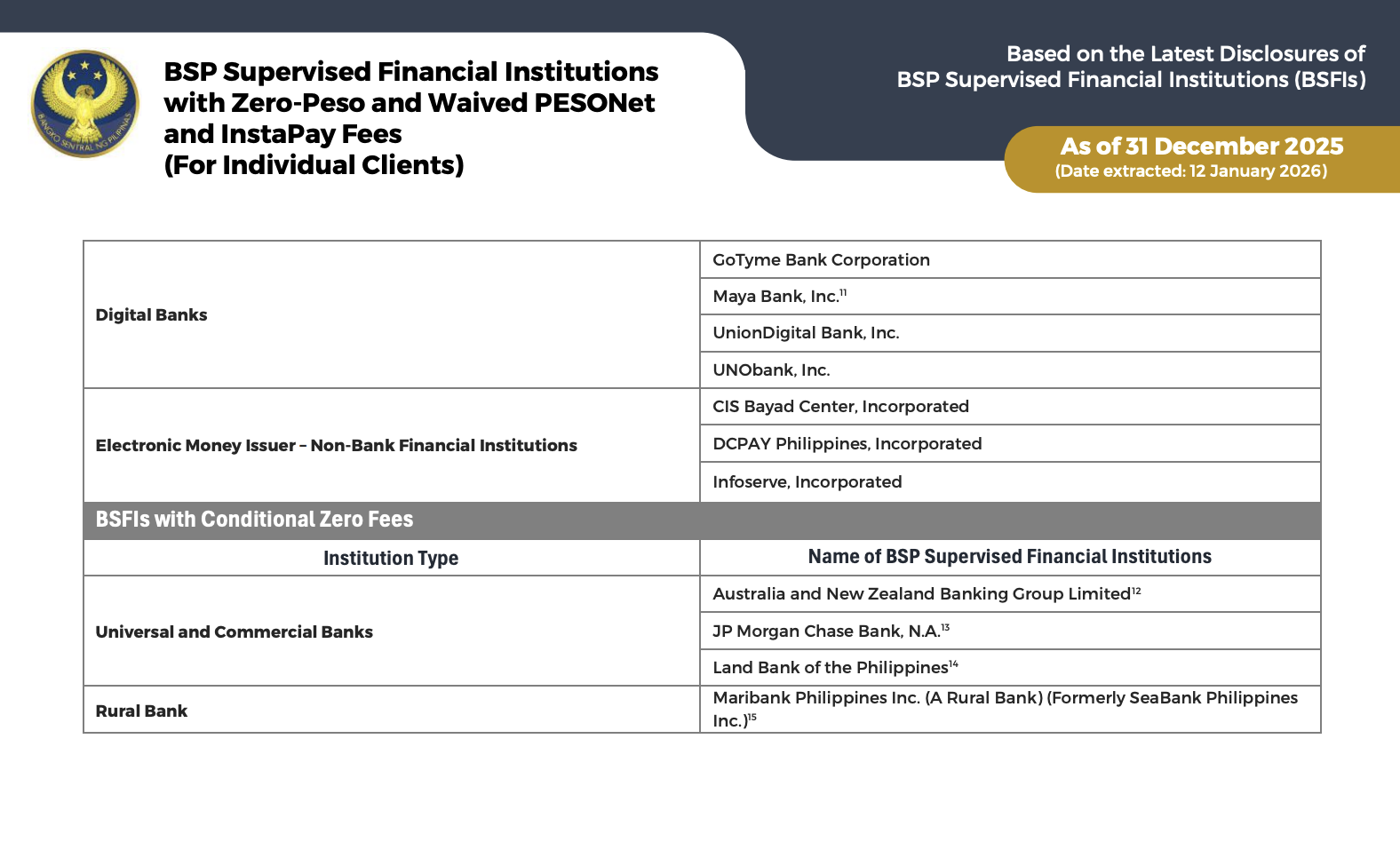

This development aligns with the Bangko Sentral ng Pilipinas’ broader push to standardize and more closely supervise electronic payment channels such as InstaPay and PESONet. Recent BSP circulars have strengthened oversight of these automated clearing houses, while published fee matrices show how banks are expected to disclose and rationalize charges for digital transfers, including zero‑fee tiers and volume‑based pricing. Industry observers note that proprietary “linked account” cash‑in options have been gradually giving way to more transparent, ACH‑based transfers governed under BSP rules.

For GoTyme customers, the loss of in‑app linked deposits means an extra step when moving funds, as transfers must now be initiated from the sending bank’s app instead of within GoTyme itself. The impact on costs will depend on each user’s primary bank and how many free InstaPay or PESONet transactions that bank offers, but some may see higher or more frequent fees versus the previous limited free linked deposits. Despite the inconvenience, regulators and payments experts argue that the shift should result in more consistent consumer protection and clearer pricing across digital channels in the long run.

For GoTyme customers, the loss of in‑app linked deposits means an extra step when moving funds, as transfers must now be initiated from the sending bank’s app instead of within GoTyme itself. The impact on costs will depend on each user’s primary bank and how many free InstaPay or PESONet transactions that bank offers, but some may see higher or more frequent fees versus the previous limited free linked deposits. Despite the inconvenience, regulators and payments experts argue that the shift should result in more consistent consumer protection and clearer pricing across digital channels in the long run.

0 Comments

Leave a Reply