The way Filipinos move money between banks and e‑wallets is quietly undergoing its biggest policy shake‑up since InstaPay and PESONet launched. New rules from the Bangko Sentral ng Pilipinas (BSP) and industry guidance from the Philippine Payments Management, Inc. (PPMI) are pushing digital banks and e‑wallets to rely more on standardized payment rails—and less on proprietary “shortcut” integrations.

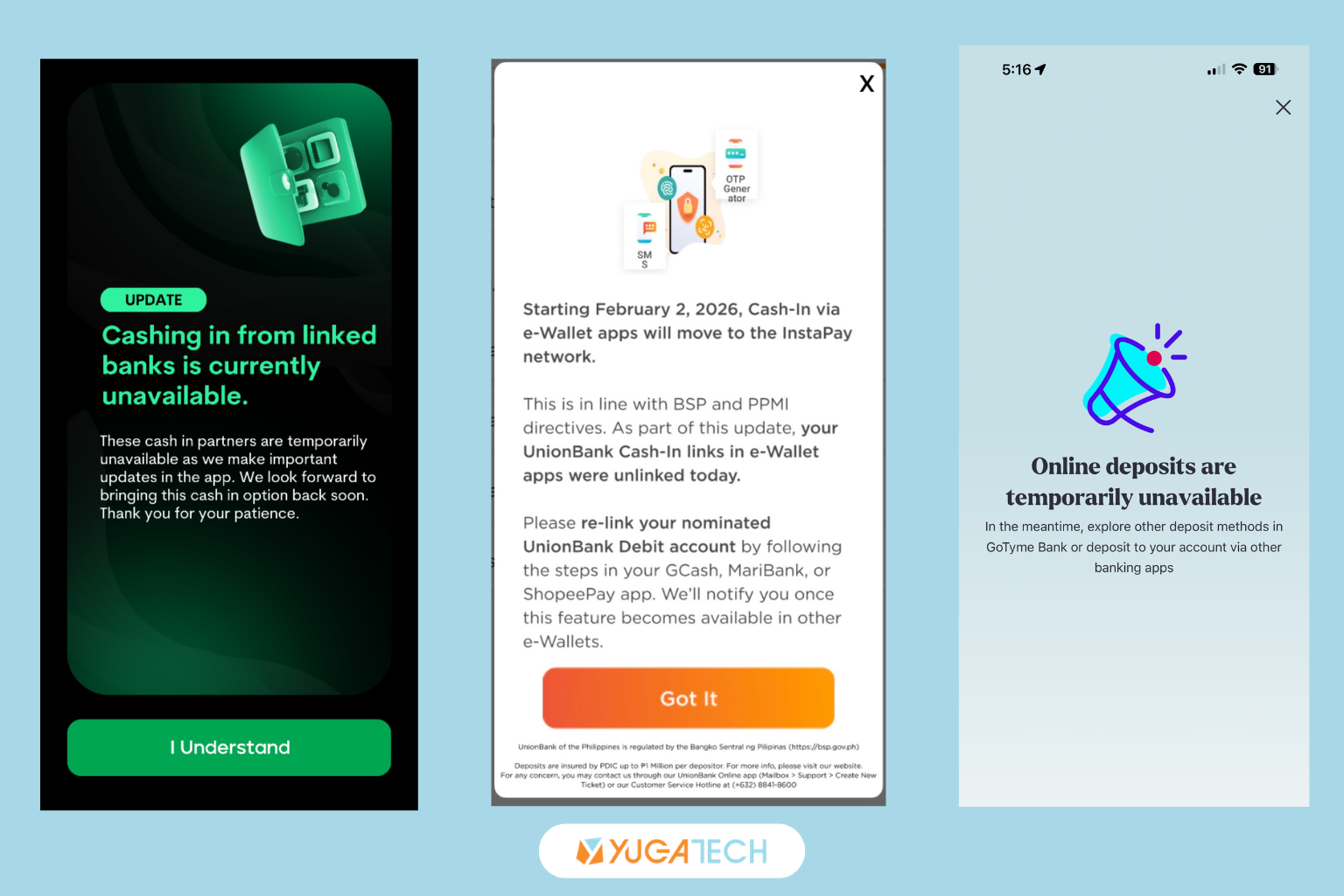

One of the clearest examples is GoTyme Bank. Starting February 1, 2026, the digital bank permanently disabled deposits via linked bank accounts “in accordance with PPMI and BSP regulations,” effectively killing a feature that allowed direct, in‑app cash‑ins from local banks such as BPI. Instead of tapping a linked account inside the GoTyme app, customers now have to send money using InstaPay or PESONet from their other bank’s mobile app, or resort to over‑the‑counter partners and cash‑in points.

![]()

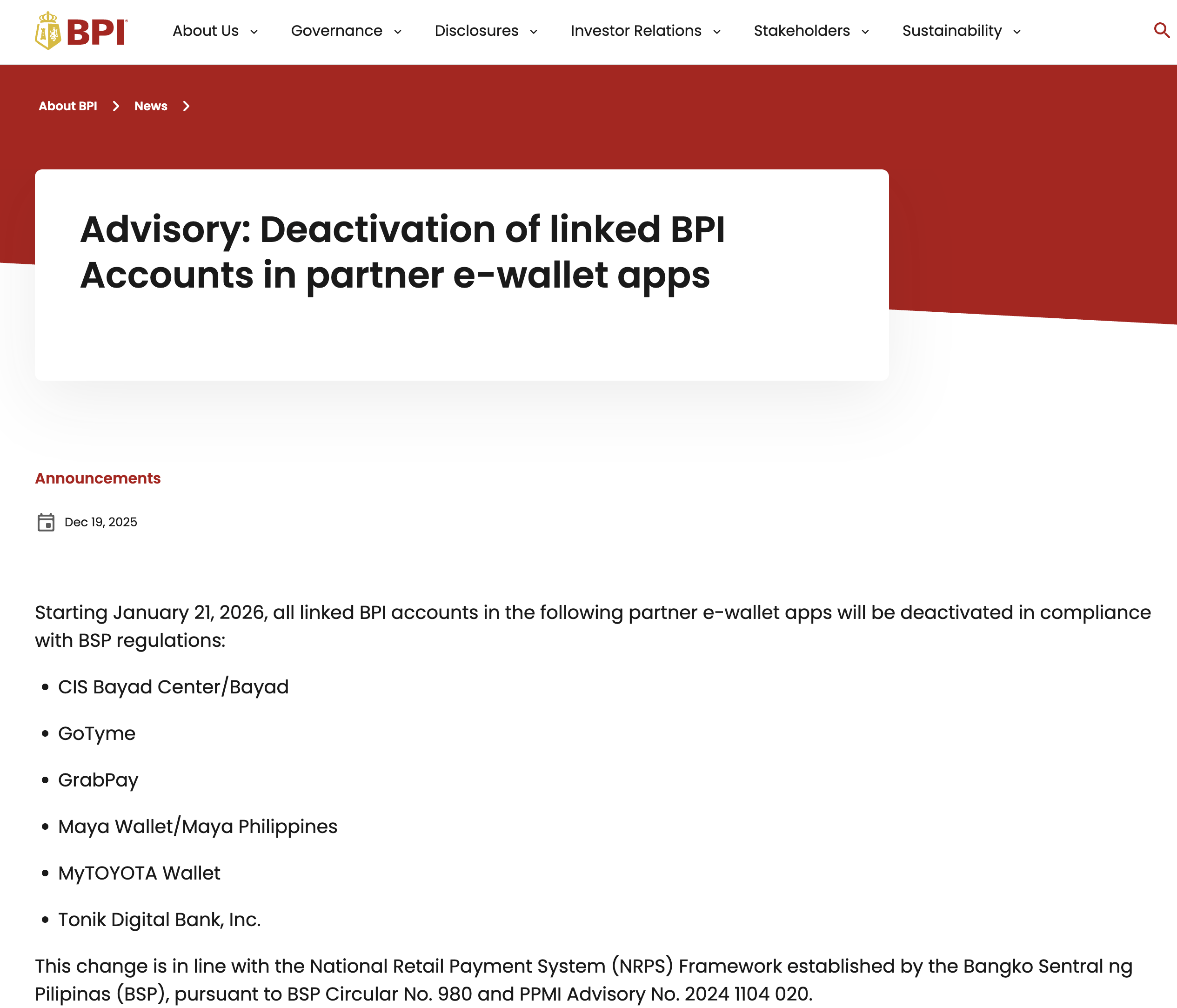

BPI is making similar moves. In a December 2025 advisory, the bank announced that all linked BPI accounts in partner e‑wallet apps—including GoTyme, GrabPay, Maya, MyToyota Wallet, Tonik, and others—will be deactivated starting January 21, 2026, explicitly “in compliance with BSP regulations” under the National Retail Payment System framework and a PPMI advisory. BPI is steering customers toward InstaPay transfers instead, reinforcing the central bank’s preference for regulated, interoperable rails over custom links.

Behind these visible changes is a broader upgrade of the country’s digital payment infrastructure. BSP’s enhanced rules for InstaPay and PESONet settlements give the central bank more power to scrutinize how funds are cleared and credited, improving resilience while enabling shorter clearing intervals and faster posting of funds. Updated guidelines also set industry‑wide expectations for participating banks and electronic money issuers, from risk controls to service delivery standards for electronic transfers.

For end‑users, the impact is mixed but significant. On one hand, convenience features like “two free deposits via linked accounts” or one‑tap in‑app cash‑ins are disappearing, forcing customers to juggle multiple apps and, in some cases, pay more frequent InstaPay or PESONet fees. On the other hand, the same rules are designed to make digital banking more predictable. BSP now requires banks and EMIs to refund failed InstaPay and PESONet transfers within hours instead of days, reducing the stress around stuck transactions and nudging institutions to modernize their back‑end systems.

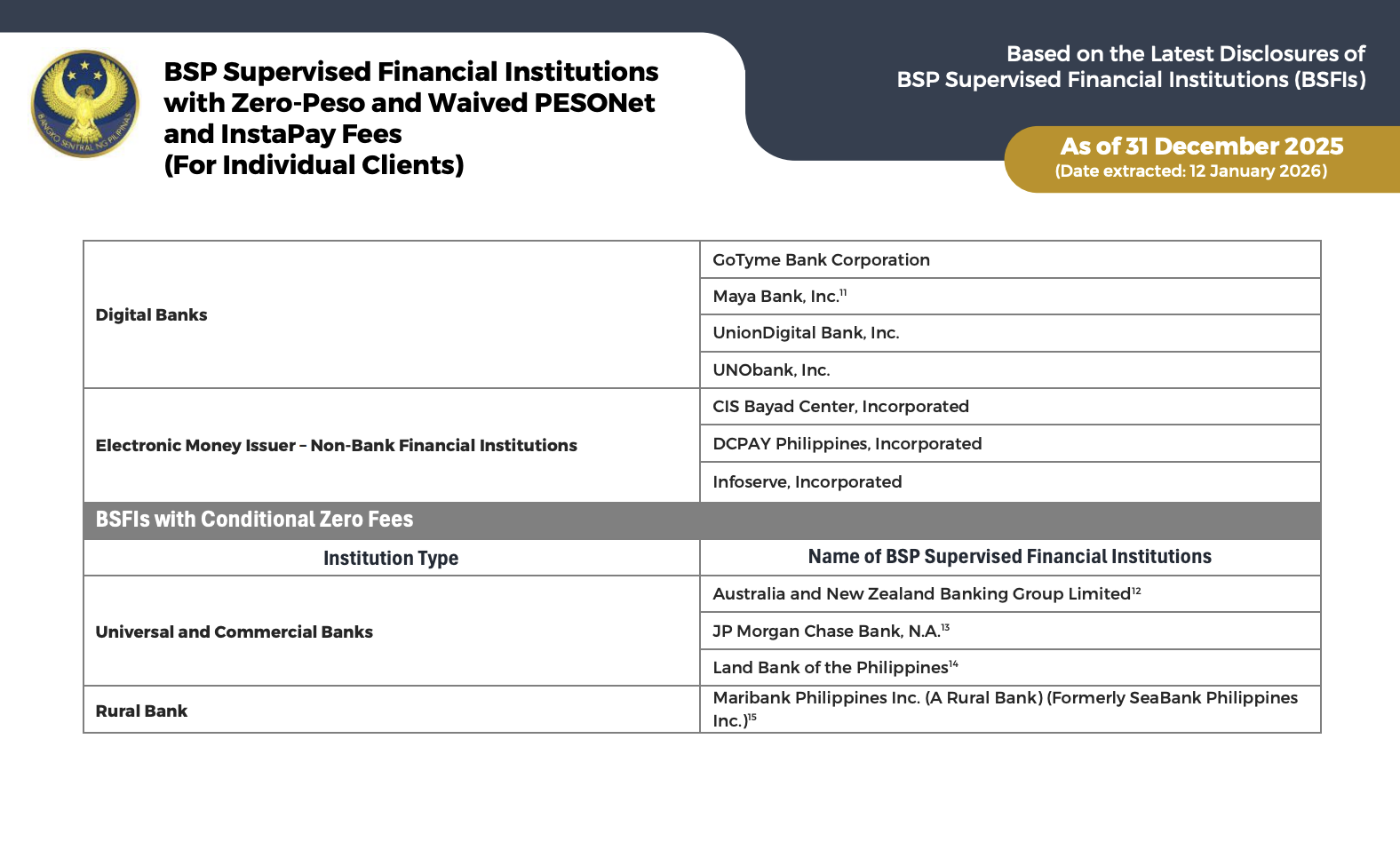

There is also a clear push for transparency. BSP regularly publishes fee matrices for PESONet and InstaPay, showing which institutions offer zero‑peso or discounted transfers and which still charge higher amounts. As more cash‑ins and cash‑outs are routed through these regulated channels, users can more easily compare costs across banks and wallets and adjust their habits accordingly—for example, timing high‑value transfers to cheaper channels or choosing banks with more generous free transfer quotas.

In the bigger picture, the deactivation of linked bank accounts in apps like GoTyme and the tightening of InstaPay/PESONet rules point to the same direction: a digital payments ecosystem that is open, interoperable, and governed by common standards, rather than one built on exclusive, opaque arrangements. The trade‑off is that some of the most convenient, “hidden” integrations are going away. In exchange, Filipinos get clearer protections, faster refunds, and a more level playing field for banks, digital banks, and e‑wallets competing for their transactions.

0 Comments

Leave a Reply